Semiconductor Price Surge 2025–2026: A Deep Dive into Rising Electronic Component Costs

The global semiconductor industry is entering a new phase of structural inflation. Between 2025 and 2026, electronic component prices—from memory chips to advanced logic ICs—have experienced significant year-over-year (YoY) increases. Unlike previous cyclical spikes, this surge is being driven by structural demand shifts, particularly from artificial intelligence (AI), data centers, and advanced computing.

This Simplytronix report analyzes pricing trends across major IC manufacturers, supported by public industry data and market intelligence.

1. Global Semiconductor Market Growth vs Price Inflation

The semiconductor industry has expanded rapidly, but much of the revenue growth is driven by price increases rather than unit shipments.

| Year | Global Market Size | YoY Growth | Key Driver |

|---|---|---|---|

| 2024 | $630B (approx.) | - | Recovery phase |

| 2025 | $772–792B | ~22–25% | AI demand surge |

| 2026 (forecast) | $854B – $1T | 10–25% | Price-driven growth |

Industry data confirms that 2025 growth was largely driven by pricing (ASP increases), not volume expansion. :contentReference[oaicite:0]{index=0}

2. Foundry Price Increases (TSMC, Samsung, Intel)

Leading semiconductor foundries are increasing wafer pricing due to massive capital expenditures and advanced node costs.

| Manufacturer | Node | YoY Price Increase (2025–2026) | Key Reason |

|---|---|---|---|

| TSMC | 3nm / Advanced Nodes | +3% to +10% | High capex ($40–56B) |

| Samsung Foundry | 3nm / 2nm | +5% to +10% | Yield + competition |

| Intel Foundry | 18A / Advanced | Rising (undisclosed) | US fab investments |

Major foundries are passing rising fabrication costs downstream, impacting all semiconductor-based products. :contentReference[oaicite:1]{index=1}

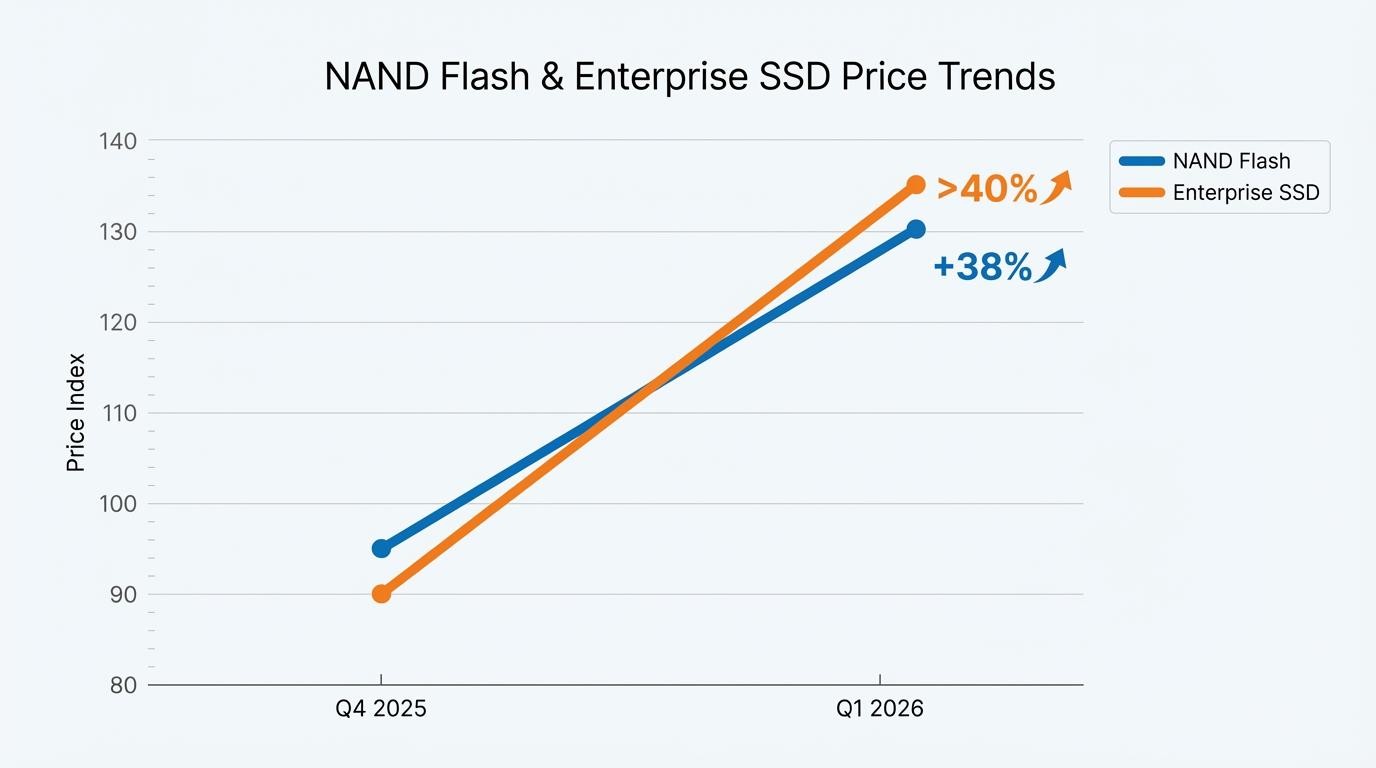

3. Memory IC Price Explosion (DRAM & NAND)

Memory components have seen the most dramatic price increases in the current cycle.

| Component | YoY Price Change | Short-Term Spike | Primary Cause |

|---|---|---|---|

| DRAM | +40% to +75% | Up to +95% QoQ | AI server demand |

| NAND Flash | +20% to +60% | Doubling in some cases | Storage demand surge |

| HBM (AI Memory) | >+100% | Severe shortage | AI GPUs |

Reports indicate memory price increases are so significant that up to 45% of Big Tech capex growth is purely due to rising component costs. :contentReference[oaicite:2]{index=2}

TrendForce also reported DRAM prices jumping up to 90–95% in early 2026 due to supply shortages. :contentReference[oaicite:3]{index=3}

4. CPU, MCU, and Analog IC Pricing Trends

Price increases are no longer limited to memory—logic and analog components are also rising.

| Category | YoY Price Trend | Market Observation |

|---|---|---|

| CPUs | +5% to +15% | AI and server demand |

| Microcontrollers (MCUs) | +5% to +12% | Automotive recovery |

| Analog ICs | Flat to +5% | Stable but rising input costs |

Multiple manufacturers, including Chinese IC suppliers, have announced price hikes across NOR flash and controller segments. :contentReference[oaicite:4]{index=4}

5. Root Causes Behind the Price Increase

5.1 AI-Driven Demand Shock

AI infrastructure is the single largest driver of semiconductor demand. AI chips alone are expected to approach $500 billion in revenue in 2026. :contentReference[oaicite:5]{index=5}

5.2 Capital Expenditure Explosion

Leading manufacturers are investing tens of billions annually:

- TSMC: Up to $56 billion in 2026 capex

- New fabs costing $15–20 billion each

5.3 Supply Chain Constraints

Geopolitical tensions, export controls, and material shortages continue to disrupt supply chains.

5.4 Advanced Node Economics

Sub-5nm fabrication dramatically increases cost per wafer, forcing manufacturers to raise prices.

6. ASP (Average Selling Price) Trend Analysis

| Segment | ASP Trend 2025 | ASP Trend 2026 | Outlook |

|---|---|---|---|

| Logic IC | ↑ Moderate | ↑ High | AI-led growth |

| Memory | ↑ High | ↑ Very High | Shortage-driven |

| Analog | → Stable | ↑ Slight | Cost pressure |

Industry analysts confirm that current growth is ASP-led, meaning pricing—not volume—is the primary revenue driver. :contentReference[oaicite:6]{index=6}

7. Impact on Electronics Industry

- Consumer Electronics: Rising smartphone, laptop, and SSD prices

- Automotive: Increased EV and ADAS system costs

- Industrial: Higher BOM costs affecting margins

- Data Centers: Massive capex inflation

DDR5 memory prices have increased up to 4× since mid-2025, and SSD prices have doubled in some markets. :contentReference[oaicite:7]{index=7}

8. Regional Trends

| Region | Trend | Insight |

|---|---|---|

| Asia-Pacific | Highest growth | Manufacturing hub |

| USA | Rising costs | Domestic fab expansion |

| Europe | Moderate growth | Automotive demand |

9. Outlook: Will Prices Continue Rising?

Short-term outlook (2026–2027):

- Prices expected to remain elevated due to AI demand

- Memory shortages likely to persist

- Foundry pricing will continue upward trend

Long-term outlook (post-2027):

- Possible correction as new fabs come online

- Competition may stabilize pricing

- Next supercycle expected post-2029

Conclusion

The 2025–2026 semiconductor price surge marks a structural shift rather than a temporary spike. Driven by AI, supply constraints, and rising manufacturing costs, electronic component prices are likely to remain elevated in the near term.

For OEMs, distributors, and procurement teams, this means adapting strategies—securing long-term supply contracts, diversifying sourcing, and optimizing BOM design.

At Simplytronix, we continue to monitor global semiconductor trends to help businesses navigate pricing volatility and ensure supply chain resilience.